October 21, 2013

Posted in Uncategorized tagged congress, growth rate, Robert Barone, uncategorized at 8:37 PM by Robert Barone

A few things became clearer during the recently ended federal government “shutdown” and debt ceiling crisis:

1. Our political system has deteriorated to the point where each side of the political spectrum is willing to push to the very brink of disaster before even the most basic remedial action is taken.

2. The “level” of the debt is really not the issue; it is the growth rate of that debt relative to the growth of the economy.

These issues raise the level of uncertainty in the economy and therefore stymie private-sector growth and job creation.

Spending projections

All credible projections of federal spending show that Social Security, Medicare/Medicaid and other social spending programs will explode in the coming years unless Congress and the president do something to fix the situation.

In 1982, projections were that Social Security faced insolvency by 1990. But, that didn’t happen because President Reagan and House Speaker Tip O’Neill reached a compromise and a solutionthat kept the Social Security program viable for a while longer.

To the brink

When Congress and the president confront the spending issues, their choices will be to raise taxes, reduce benefits or, via compromise, some combination of the two.

But we know that they won’t act until the spending issues become a recognizable crisis and/or their political futures require that they act. This is most likely to come in the form of “invisible hand” economic actions wherein the dollar drops in value relative to other currencies and interest rates rise, as the international community relies less and less on the dollar as the world’s reserve currency.

China and Russia are becoming more and more vocal and active in seeking alternatives to the dollar in world trade. If the necessary spending controls aren’t soon put in place, the U.S. economy could lose its premier status. Don’t underestimate the importance of the “reserve currency” status in the economic growth equation.

The reality of the debt

One argument in the current bickering is that the country will never be able to repay the $17 trillion of debt it has accumulated. From an economic point of view, the debt level itself isn’t the issue. The issue is how fast that debt is growing and its cost.

Unlike an individual whose debts all come due upon death(either the estate pays the debt off or the lender(s) writes it off), a country doesn’t die (without a revolution). As long as the growth rate of the debt is less than the growth rate of the economy, and as long as interest rates remain reasonable, the debt will never be expected to be repaid.

From this point of view, the most significant single statistic is the debt’s relationship to GDP. The concept is similar to that of an application for a mortgage. The borrower needs a reasonable “debt payment/income ratio” to qualify. The more pre-existing debt one has, and the more of one’s income it takes to service that debt, the less credit worthy the individual becomes.

Debt/GDP history

After World War II, the debt/GDP ratio was 120 percent. Why wasn’t it a disaster then? The answer: 1) the war had ended and spending was reduced; and 2) the economy grew faster than the debt.

By 1974, the debt/GDP ratio had fallen to 32 percent. It rose after that to 66 percent in 1996 after the recession of the early ’90s, but fell to 56 percent during the strong economic growth years of the late ’90s and the spending-control emphasis of the Congress (which was accepted and then embraced by President Bill Clinton).

By 2008, as a result of the 2001 recession and debt growth outpacing economic growth during the Bush presidency, the ratio rose to 70 percent. Then came the financial crisis and the recession with weak economic growth in its aftermath. The debt/GDP ratio now stands at more than 100 percent, a level that makes the international community nervous.

Conclusion

There are two key concepts here: 1) controlling the size of the fiscal deficit to control the growth rate of the debt (this implies confronting the growth rate of the social programs); and 2) growing the economy fast enough to accommodate a rising level of debt.

Spending, entitlement growth, the growth of the debt and economic growth are all intertwined. Since the spending issues were taken off the table in this week’s debt ceiling bill, the only chance at avoiding a true debt crisis is for the economy to grow.

The so-called “resolution” reopens the government only through Jan. 15 and increases the debt ceiling only until Feb. 7. Businesses are asking, “Are we going to relive this debacle all over again in three months?”

Such uncertainty clearly shows up in all of the business surveys as holding back economic growth and job creation. For everyone’s benefit, it behooves Washington to put some degree of certainty back into the business markets, at least for a long-enough time period to allow a return on new capital deployment.

The longer-term question is whether or not federal spending growth will allow the debt/GDP ratio to decline. If it does, then the fiscal issues in Washington, D.C., will disappear, just as they did post-World War II.

Unfortunately, the current way the government runs almost guarantees that spending will continue to probe the limits of the debt/GDP ratio. If this doesn’t change, one might want to prepare for those “invisible hand” economic implications.

Robert Barone (Ph.D., economics, Georgetown University) is a principal of Universal Value Advisors, Reno, a registered investment adviser. Barone is a former director of the Federal Home Loan Bank of San Francisco and is currently a director of Allied Mineral Products, Columbus, Ohio, AAA Northern California, Nevada, Utah Auto Club, and the associated AAA Insurance Co., where he chairs the investment committee. Barone or the professionals at UVA (Joshua Barone, Andrea Knapp, Matt Marcewicz and Marvin Grulli) are available to discuss client investment needs.

Call them at 775-284-7778.

Statistics and other information have been compiled from various sources. Universal Value Advisors believes the facts and information to be accurate and credible but makes no guarantee to the complete accuracy of this information.

Permalink

October 16, 2013

Posted in Economy, Robert Barone, Uncategorized tagged Debt, GDP at 9:48 PM by Robert Barone

All credible projections of federal spending show entitlements, especially Social Security and Medicare/Medicaid, exploding in coming years — unless, that is, Congress and the President do something to fix the situation.

In 1982, projections were that Social Security faced insolvency by 1990. But that didn’t happen because President Reagan and House Speaker Tip O’Neill reached a compromise and a solution that kept the Social Security program viable for a while longer.

Today, due to demographic and other factors, the growth rate of Social Security, Medicare/Medicaid and the other entitlements has budget-busting and debt-level implications that have caused consternation and uncertainty in the business community and financial markets.

When Congress and President Obama will be forced to confront the spending issues, their choices will be: raising taxes, reducing benefits or, via compromise, some combination of the two. But we know they won’t act until the spending issues become a recognizable crisis and their political futures require action.

This is most likely to come in the form of “invisible hand” economic actions wherein the dollar drops in value relative to other currencies and interest rates rise as the international community relies less and less on the dollar as the world’s reserve currency. If that doesn’t cause enough political pressure to bring about the necessary spending controls, then the U.S. economy may well lose its premier status.

The Reality of the Debt

One argument in the current bickering is the country will never be able to repay the $17 trillion of debt it has accumulated. From an economic point of view, the debt level itself isn’t the issue. The issue is how fast that debt is growing and its cost.

Unlike an individual whose debts all come due upon death (either the estate pays the debt off, or the lender(s) writes it off), a country doesn’t die. As long as the growth rate of the debt is less than the growth rate of the economy, and as long as interest rates remain reasonable, the debt will never have to be repaid. From this point of view, the most significant single statistic with regard to the debt is its relationship to GDP.

The concept is similar to that of an application for a mortgage. The borrower needs a reasonable “debt payment/income ratio” to qualify. The more pre-existing debt one has, and the more of one’s income it takes to service that debt, the less creditworthy the individual becomes.

After World War II, the debt to GDP ratio was 120%. Why wasn’t it a disaster then? The answer: 1) the war had ended and spending was reduced and 2) the economy grew faster than the debt. By 1974, the debt to GDP ratio had fallen to 32%. It rose after that, to 66% in 1996 after the recession of the early 1990s. Then it fell to 56% during the strong economic growth years of the late 1990s and the spending control emphasis of the Congress — which was accepted and then embraced by President Clinton.

By 2008, as a result of debt growth outpacing economic growth during the George W. Bush presidency, the ratio rose to 70%. Then came the financial crisis and Great Recession, with weak economic growth in its aftermath. The debt to GDP ratio now stands at more than 100%, a level that makes the international community nervous.

Conclusion

There are two key concepts here: 1) controlling the size of the fiscal deficit to control the growth rate of the debt (this implies confronting the entitlement growth issues) and 2) growing the economy fast enough to accommodate a rising level of debt (which implies that the rate of economic growth be faster than the growth rate of the debt).

Spending, entitlement growth, the growth of the debt and economic growth are all interrelated. If confronting the entitlement issues is off the table in the current political negotiations, as it appears to be, then the only chance at avoiding a true debt crisis is for the economy to grow.

The longer the politicians bicker about the budget, taxes and spending, the more that uncertainty will hold back economic growth. That clearly shows up in all of the business surveys.

For everyone’s benefit, it behooves Washington to put some degree of certainty back into the business markets, at least for a time period that will allow a return on new capital deployment.

The longer-term question is whether or not federal spending growth will allow the debt to GDP ratio to decline. If it does, then the fiscal issues in Washington will disappear, just as they did post-World War II. If it doesn’t, one should prepare for those “invisible hand” economic implications.

Robert Barone (Ph.D., economics, Georgetown University) is a principal of Universal Value Advisors, Reno, a registered investment adviser. Barone is a former director of the Federal Home Loan Bank of San Francisco and is currently a director of Allied Mineral Products, Columbus, Ohio, AAA Northern California, Nevada, Utah Auto Club, and the associated AAA Insurance Co., where he chairs the investment committee. Barone or the professionals at UVA (Joshua Barone, Andrea Knapp, Matt Marcewicz and Marvin Grulli) are available to discuss client investment needs.

Call them at 775-284-7778.

Statistics and other information have been compiled from various sources. Universal Value Advisors believes the facts and information to be accurate and credible but makes no guarantee to the complete accuracy of this information.

Permalink

October 8, 2013

Posted in government, Robert Barone, Uncategorized tagged employment, shutdown at 4:37 PM by Robert Barone

I was quite surprised when I got up last Tuesday to find that all of my utilities were working, including TV; my trash had been picked up; and, when I drove to work, the traffic lights were operating, the schools were open and I even spotted a couple of local police patrol cars.

It appeared to be a normal Tuesday morning.Well, I wasn’t really surprised. But I would have been if I believed the media’s vision, which had built to a crescendo on Monday, that the so-called “shutdown” was going to be an unmitigated disaster.

By Wednesday, as far as I could tell, the national parks had closed, as had some museums and monuments in Washington, D.C. I am also informed that some data releases (like September’s unemployment rate) will be delayed. But, all in all, there hasn’t been much impact on my daily life and probably not on yours, either.

Now, I am not making light of the issue, as it will definitely have an impact if prolonged. (Actually, the upcoming debt ceiling issue has much more potential to do damage.) But the fact that there was no real immediate impact on most Americans’ lives makes one realize that state and local government services play a much larger role in our daily lives than federal government services do.

Government approaches

Since the financial crisis, governments at all levels have struggled either because they cannot control spending or, more likely, have made future commitments that they simply cannot meet.

During such times of financial stress, state and local governments typically take one of two approaches, or even a combination:

• The preferred approach is for government to work with the private sector to promote business and employment growth. In the long run, a healthy and growing private sector generates more tax revenue. You don’t have to raise the rates to accomplish this.

• The second way, which is simply wrongheaded, is to increase taxes and fees on the current citizenry. In the long run, this drives business away and the revenue issues remain or even get worse.

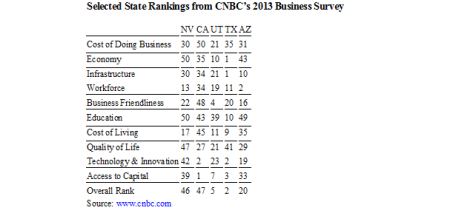

CNBC survey

Every year, CNBC and others such as Forbes do surveys of which states are best for private-sector businesses.The accompanying table shows the results of the 2013 CNBC survey for the Western states with which Nevada competes for business relocations (Arizona, Utah, Texas). I also threw in California because many relocations originate there. Nevada’s overall ranking is 46th out of 50. Nevada has been ranked between 45 and 47 at least since ’08.

Looking at the table, Nevada generally ranks poorly in every category, most notably economy, education, quality of life and technology and innovation.

Nevada’s lackluster record

To its credit, the governor and the Nevada Legislature approved a $10 million fund that targets cutting-edge technologies, modeled after a similar and successful effort in Utah.

But state and local governments can do much more. Economic growth in the state would improve if officials reduced the cost of being in business and improved business friendliness via a reduction in fees and regulations. I estimate that if such improvements were made, the state could move up significantly in the CNBC survey.

Some would think this impossible. Not so. Despite the Detroit bankruptcy, over the last four years, state and local governments in Michigan have moved that state from a rank of 41st (’09) to a rank of 29th in the latest survey. There, governments aggressively go after business relocations and become partners, not antagonists.

The record in Nevada is not good. Except for the cutting-edge technology fund, state and local legislators have opted for raising fees and taxes. Here are some examples:

• Since the financial crisis, the state has doubled the business license fee, and most of the local governments have followed suit.

• Assembly Bill 46, passed by the recent “no new taxes” Legislature, permits the local governments to raise taxes without the constitutional requirement of a two-thirds vote of the Legislature. While its constitutionality has yet to be tested, AB46 is an example of how government works today — by sleight of hand.

• In Reno, it costs more than $50,000 in permit fees to build a 3,000-square-foot building.

• Anyone who owns a small business in Northern Nevada can attest to the significant increase in fees and regulations since the crisis.

Conclusion

We are lucky that California is our neighbor, as it ranks last in the cost of doing business, is 48th out of 50 in business friendliness and 45th in cost of living. Overall, it is ranked 47th, one place lower than Nevada. And, while businesses are leaving California in droves and some are relocating to Nevada, the state could be getting a much larger share if it was more business-friendly.

Robert Barone (Ph.D., economics, Georgetown University) is a principal of Universal Value Advisors, Reno, a registered investment adviser. Barone is a former director of the Federal Home Loan Bank of San Francisco and is currently a director of Allied Mineral Products, Columbus, Ohio, AAA Northern California, Nevada, Utah Auto Club, and the associated AAA Insurance Co., where he chairs the investment committee. Barone or the professionals at UVA (Joshua Barone, Andrea Knapp, Matt Marcewicz and Marvin Grulli) are available to discuss client investment needs.

Call them at 775-284-7778.

Statistics and other information have been compiled from various sources. Universal Value Advisors believes the facts and information to be accurate and credible but makes no guarantee to the complete accuracy of this information.

Permalink

Posted in business, Robert Barone, Uncategorized tagged Middle East, sales results at 3:47 PM by Robert Barone

The markets have been fixated on the political standoff in Washington, D.C. Through Friday, October 4th, the S&P 500 was down in 9 of its last 12 sessions. The uncertainty, especially over the debt ceiling and possible “default,” has made investors hesitant to make longer-term commitments with their investible funds. Nevertheless, the data from the private sector, especially of late, has been much stronger than earlier in the year.

Consider:

The manufacturing sector is hot. The Institute for Supply Management (ISM) manufacturing index was 56.2 in September, the highest in nearly 2.5 years. In the U.S., we are seeing a manufacturing renaissance as labor cost increases in China and much of Asia are running in excess of 10% annually. As an example of what is going on in manufacturing, 9 of GM’s 17 production plants are operating flat out on an around the clock (3 shift) schedule. In 2008, at the last auto peak, only 3 of the then 20 plants were operating at full capacity. In August, auto sales were 16.1 million units (SAAR – seasonally adjusted annual rate), a level not seen since before the financial crisis. Sales fell back in September to 15.3 million units (SAAR) but only because the Labor Day holiday was on Monday, September 2nd and some weekend sales were pulled into the August numbers. The average of the two months, 15.7 million units (SAAR) isn’t anything to sneer at.

In the labor markets, employers are having a hard time finding qualified applicants. This is quite a different market than it was even 2 years ago. First time filers for unemployment insurance are at levels not seen since ’07, and this particular economic series has a high inverse correlation with stock prices, i.e., when claims fall, stock prices rise. Voluntary quits are also up significantly indicating that current employees are getting more confident that they can find new employment. And, despite the secular downtrend in the labor force participation rate, a labor shortage is developing.

While suffering a setback due to higher mortgage rates this summer, the housing market still suffers from a lack of supply. This isn’t surprising given that we have had only minimal new housing construction for the past half decade while population growth has continued. As a result, there has been a double digit rise in home values over the past 12 months, which makes middle class homeowners more confident and more willing to spend and take on debt. We see this in the consumer sentiment surveys, in the growth of credit card debt, and in new auto financings

The U.S. economy is mainly service based, so the ISM non-manufacturing index is an important indicator of economic health. In August, that index hit 62.2, the highest level since early 2011, a time when GDP was expanding faster than 3%. Not to get too excited, the index fell back to 55.1 in September. Nevertheless, that is still a healthy result. By definition, anything over 50.0 signals growth.

The worry over China (which embodies Australia, Canada, and others which supply China much of its raw materials) now seems overdone. While economic growth is much lower than in the past decade, 7.5% is still much faster than anything the mature economies could hope for. There was no “hard landing” there, and indications are that growth has resumed. This is positive for exports and international large cap companies. In addition, Europe’s economy appears to have bottomed.

Meanwhile, the Federal Reserve and other central banks have kept the monetary spigots open, and, because of the so-called “crisis” issues in Washington, D.C., it seems unlikely that Bernanke will begin to “taper” money before year’s end. In addition, and just as an historical note, in the post-WWII era, every recession has been preceded by a significant “tightening” of monetary policy (i.e., yield curve inversion where short-term rates are higher than long-term ones). As indicated above, it appears we are a long way from that. Normally, when the economy grows and monetary policy is still easy, stock prices rise.

Don’t get me wrong. The long-term outlook is still clouded. Middle East tensions persist, terrorism, led by Al-Qaeda, is not dead, and U.S. influence in the world is waning. In addition, the long-term struggle with debt, its costs, and entitlements in the U.S. and Europe still hasn’t been dealt with. Nor has risk in the financial system been removed. This is true for the U.S., but especially true for Europe.

But, if the debt ceiling is raised without a U.S. default (which is the highly likely scenario), markets will have a relief rally, and, at least for the short-term, concerns over those nasty long-term issues will be put on the back burner. Remember, rising markets often climb a “wall of worry.” Perhaps, the political antics now playing out in Washington, D.C., especially if they push the default issue to the precipice, will ultimately give investors a buying opportunity in the equity markets.

Robert Barone (Ph.D., economics, Georgetown University) is a principal of Universal Value Advisors, Reno, a registered investment adviser. Barone is a former director of the Federal Home Loan Bank of San Francisco and is currently a director of Allied Mineral Products, Columbus, Ohio, AAA Northern California, Nevada, Utah Auto Club, and the associated AAA Insurance Co., where he chairs the investment committee. Barone or the professionals at UVA (Joshua Barone, Andrea Knapp, Matt Marcewicz and Marvin Grulli) are available to discuss client investment needs.

Call them at 775-284-7778.

Statistics and other information have been compiled from various sources. Universal Value Advisors believes the facts and information to be accurate and credible but makes no guarantee to the complete accuracy of this information.

Permalink